11.05.2026

Investment Market: Signs of Recovery After a Challenging 2025

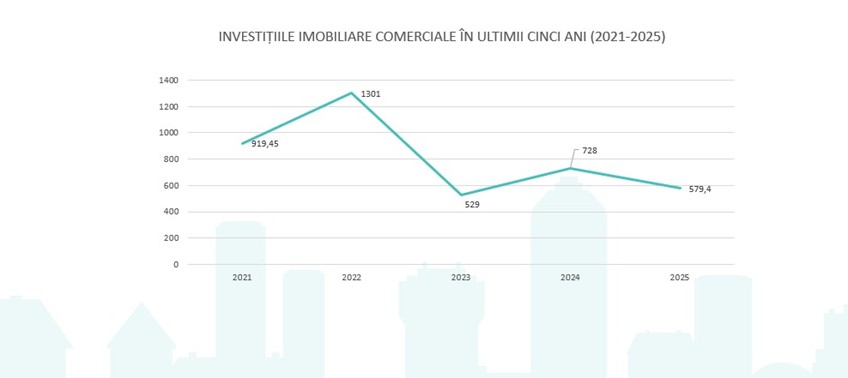

Following a 31% decline in liquidity in 2025 compared to 2024, Romania’s real estate investment market is showing the first clear signs of recovery. Last year’s slowdown largely reflected the postponement of several large-scale transactions into 2026, with the office sector leading total volumes at 40%, followed by retail at 36%. Against this backdrop, 2026 projections are optimistic: with multiple major transactions currently in advanced stages of negotiation, total investment volumes could reach approximately €900 million. Prime yields and rents remained broadly stable in Q1 2026, providing a degree of predictability for the period ahead.

Office Take-Up: Demand Softens, but the Market Rebalances

Both Bucharest and regional cities recorded declines in gross take-up in 2025 — down 23% and 27% respectively compared to 2024. The picture, however, is nuanced. In the capital, a lack of new supply kept lease renewals as the dominant transaction type, while higher-vacancy regional markets such as Timișoara saw more expansions and relocations. Prime rents remained stable across most markets, with Bucharest continuing to be the most complex, showing significant variation between assets and submarkets. Vacancy rates at national level continue to decline, signalling a gradual absorption of existing stock.

Regional Cities: Cluj and Brașov Lead the Development Pipeline

At regional level, Cluj-Napoca, Timișoara, Iași and Brașov all recorded year-on-year decreases in vacancy, with typical Class A rents ranging between €12.5 and €17 per sqm per month. While Bucharest has evolved beyond its IT-driven roots, regional cities such as Cluj and Iași remain heavily reliant on the technology sector as the primary demand catalyst. On the supply side, regional developers are proceeding cautiously, with Cluj and Brașov concentrating the majority of completions expected over the next three years.

Hybrid Working Models Are Reshaping Space Requirements

One of the most compelling sections of the iO Partners report examines the five dominant working models currently in play — ranging from Office Centric, with up to 75% maximum presence, to fully Remote, with four to five days worked from home. Companies recording office presence below 30–45% are already exploring flexible space solutions, a trend that is accelerating the adoption of flex and coworking formats. Hybrid models imply lower sharing ratios and a growing emphasis on social over individual workspaces — a shift with direct implications for how offices are configured and sized.

Flex Office: Steady Growth, Decentralisation Underway

Bucharest’s flex office stock surpassed 74,000 sqm by the end of 2025, accounting for over 2% of the total modern office stock — a meaningful threshold. Nationally, Romania now counts over 100 coworking locations, with the highest concentration in Bucharest, Brașov, Iași, Cluj and Timișoara. The emerging trend is one of decentralisation: satellite offices, regional hubs and flexible work environments that combine the benefits of remote work with professional office infrastructure. This evolution simultaneously addresses employee needs — reduced commuting, improved work-life balance — and corporate priorities, as businesses look to avoid long-term lease commitments and the high operational costs of a single central headquarters.